Digitalization is changing the world in all areas. Companies like banks are impacted by this in multiple ways because digitalization is much more than a nice website or a customer portal that allows some transactions online. Digital transformation also means digitizing internal processes, structures and decisions, and developing up-to-date business models with real added value for the customer. To meet this change in a sustainable way, a banking platform provides a perfect technological foundation.

If one considers the starting point for banks in the corporate banking sector and especially in highly complex lending scenarios, the conditions for digital transformation are often difficult. Yet, or perhaps for that very reason, there is an urgent need for action here in comparison to other industries – and also, in contrast with the private customer sector. On the one hand, banks are caught between ever-increasing regulation and ever-changing and ever-growing customer demands that require fast reaction times in terms of the customization of processes. On the other hand, historically-evolved landscapes of heterogeneous legacy systems with isolated databases make it difficult to kick-start technological advances, which happen at breakneck speed.

The good news upfront: When a lot of things are not going so well, there is great potential. This also applies to the corporate customer sector. To face the digital age, banks basically have two options.

Option 1: Proprietary IT solutions that tie up capital and resources

The first possibility is to create a new IT landscape on your own, that is, to set up a system of your own to pool data from existing databases and to automate their processing. This is possible in principle, but it involves enormous effort in terms of time, costs and resources. Projects of this size cannot be planned with any kind of precision and involve many risks due to their complexity. This is because the legacy systems are usually not very flexible, let alone modular; so a gradual modernization is difficult to realize. Therefore, only the Big Bang remains after a long project period in which neither the customers nor the employees see an improvement.

In this approach, the danger is very likely that you create a complex, new, maintenance-intensive solution that is already outdated at launch.

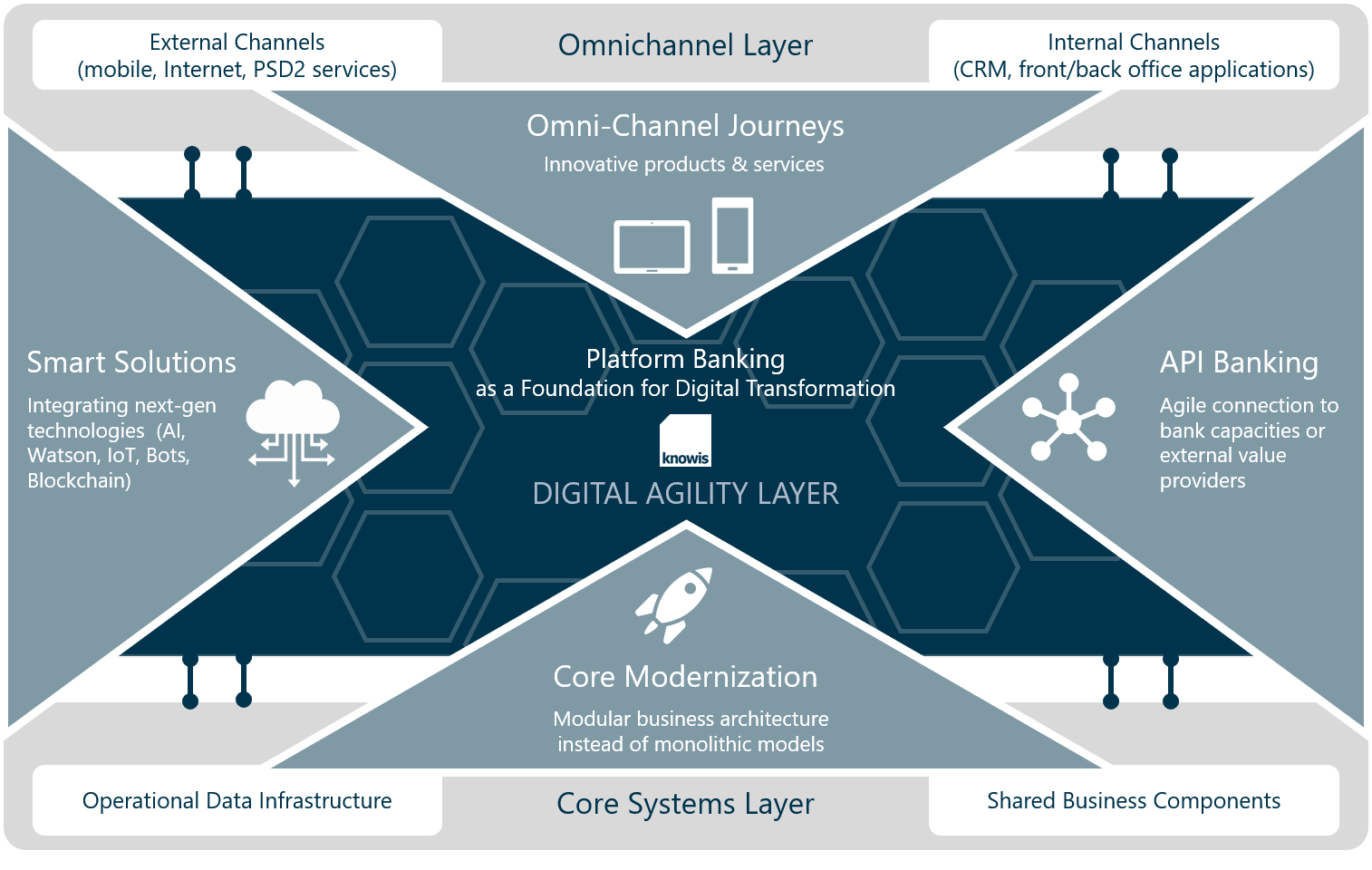

Option 2: Platform banking – The link between the frontend and the backend

The alternative is a platform banking solution that integrates with your existing systems. It acts as a connecting layer between the existing data sources as well as the internal and external user interactions and makes it possible to gradually implement new components and replace old systems. At this intermediate level ('Digital Agility Layer'), a common database is created that can be used for automated, efficient processes. Specialized software providers can design and deploy such a platform with the appropriate business applications for banks quickly and in a solution-oriented way.

In 2017, the consulting company PPI AG published the market study „Digital Banking Plattformen – Modernes Banking gestalten“. It demonstrates that the possibilities afforded by the solutions offered are well above the current market standard. Accordingly, the platforms are a good way to position themselves for the future, says Guido Köhler, a digital banking expert and Study Director at PPI AG.

Indeed, platform banking offers a whole range of advantages that can successfully lead banks through the process of digital transformation.

Linked knowledge instead of individual information

Platform banking marks the end of knowledge silos and isolated databases. Interfaces and standardized protocols make all relevant data from the existing systems available and linked. That is, information and records are no longer disjointed, but always available in the context in which they are needed. This dynamic networking provides knowledge at the push of a button that otherwise would have to be collected manually from different systems in a time-consuming process.

Moreover, networking existing information not only makes knowledge available to everyone involved in the process, but it can also lead to completely new insights that banks can use as the basis for automated processes or the implementation of innovative business applications.

Operations within the credit process can be massively accelerated

The lending cycle times are an important measure of efficiency – and as a study by the ibi Research Institute of the University of Regensburg on the future of the commercial credit process shows, almost half of the banks surveyed are not satisfied with it. Specifically, there can sometimes be more than ten days between the contract preparation and the filing of documents. Primarily, individual and manual processing steps are to blame.

Price Waterhouse Coopers (PwC) comes to the same conclusion in a study published in 2017 on the efficiency of credit processes. "As the complexity of credit products increases, so does the number of interfaces along the credit process," it says. More interfaces, longer processing times.

Platform banking allows access to all available information at all times and also supports concurrent processing and collaboration by different people. This holistic approach massively accelerates lending operations, and decisions can be made automatically where appropriate. Lending to an existing customer with manageable credit risk could be a potential use case. In more complex cases, where a detailed case-by-case assessment increases in importance, the credit experts are left with the necessary space for it. Especially when time-consuming manual activities are eliminated, more time remains for differentiating processing steps.

Third Party Collaborations Enable New Business Applications

As analyzed by PwC in the aforementioned study, many banks are still sticking to their traditional product portfolio. However, they are giving away the opportunity to differentiate themselves from their competitors, leaving new players such as fintech companies with the opportunity to create innovative offers and to capture more market share. Cooperation would be a way for banks to bring the necessary momentum into their offerings in order to keep pace with technological developments and contemporary offerings.

Thanks to modern programming standards and interfaces, platform banking solutions are compatible with third-party solutions. In this way, internal databases and legacy systems can be linked with business applications from other companies to create a value-added ecosystem for customers and banks. Interfaces accelerate the construction of new business applications by allowing modularization and, at the same time, simplification of the software. The necessary maintenance of applications is therefore also much less expensive. In addition, economies of scale are possible and the range of products can be expanded.

The customer remains in focus

Back to the roots – "The customer is king," says the old adage. He or she should be the focus of the bank, and the products and services that it makes available. In contrast to the creation of self-fabricated, monolithic solutions, which disproportionately burden internal resources, platforms that are implemented together with specialized providers allow banks the necessary space to concentrate on their core competencies and, in particular, on the customers. They can quickly be offered the digital services they expect today. The banking platform acts as a ‘digital agile layer’ between the core banking systems and the internal and external channels. All relevant information is available and is packaged for all participants and can be accessed in context.

Benefits for both sides are: In addition to the possibility of process automation, the bank gains extensive knowledge that can be used to add value in the course of the customer journey and to strengthen customer loyalty. The customer can use a variety of channels, for example, a mobile app, view or send data, and interact with the bank.

Conclusion

Digitalization is a vast evolution. Due to the deep intertwining of customer data, especially in the lending business, it is difficult for banks to break away from the old system world and reorganize on their own – the fear is great to move too far away from the customer because of resource-consuming long-term projects, the customers‘ needs and the rapid technological progress. Catching up on such a backlog will become increasingly difficult as the digital transformation progresses.

To use a gradual and modular approach to digital transformation, using a banking platform is a highly promising solution. By networking existing and emerging information, knowledge can be generated that offers great added value in the context of different processes. In this way, new business models can be created and customers can be optimally supported on their digital journey.

Image Sources: Teaser: Pinkypills - 825223420 - iStock; Infographic: knowis AG