An important success factor in projects relating to digitalization in the financial sector is to meet the requirements of the various stakeholders. Only if these groups of interest recognize a clear added value for themselves and their concerns in the project, they will support its implementation and the desired success can be achieved sustainably. Therefore, it is essential for every digitalization project in banks to identify the stakeholders, determine their needs, and take them into account at an early stage in the digital solution approach.

As in many other areas of business and industry, digital transformation also offers great potential for the financial sector. This applies to the lending business as well as to other areas such as payment transactions and investment banking. According to a study by the Frankfurt School of Finance and Management from 2016, for example, a large number of banks in German-speaking countries cannot state the exact duration for processing credit applications or the associated process costs. According to the study, the average processing time for credit applications is also eleven days. All in all: poor transparency and slow reaction times. A starting point at which significant improvements could be achieved for all parties involved - clients, the bank itself, and external third parties such as banking supervision – through digitalized processes. But how can these and other stakeholders be satisfied?

banks' Stakeholders must be in focus

Experience has shown that a step-by-step implementation of an extensive digitalization project is a very efficient approach to managing the digitalization of complex business processes. Important: The relevant internal and external stakeholders should be identified for each project phase, and their most pressing concerns should be identified and taken into account at an early stage. In other words: How can the people directly affected by the project or its results benefit from the digitized process at an early stage? The mood can turn into general rejection if no added value for the employees is discernible in medium-term. But if a modernization program creates an added value, acceptance will increase - also for all follow-up projects.

For example, when a credit process is digitalized, the clerk could be supported by

- the provision of contextual information to support decision-making,

- tools for automated cash flow calculation or

- automatically provided information from an external database

at an early stage of the project.

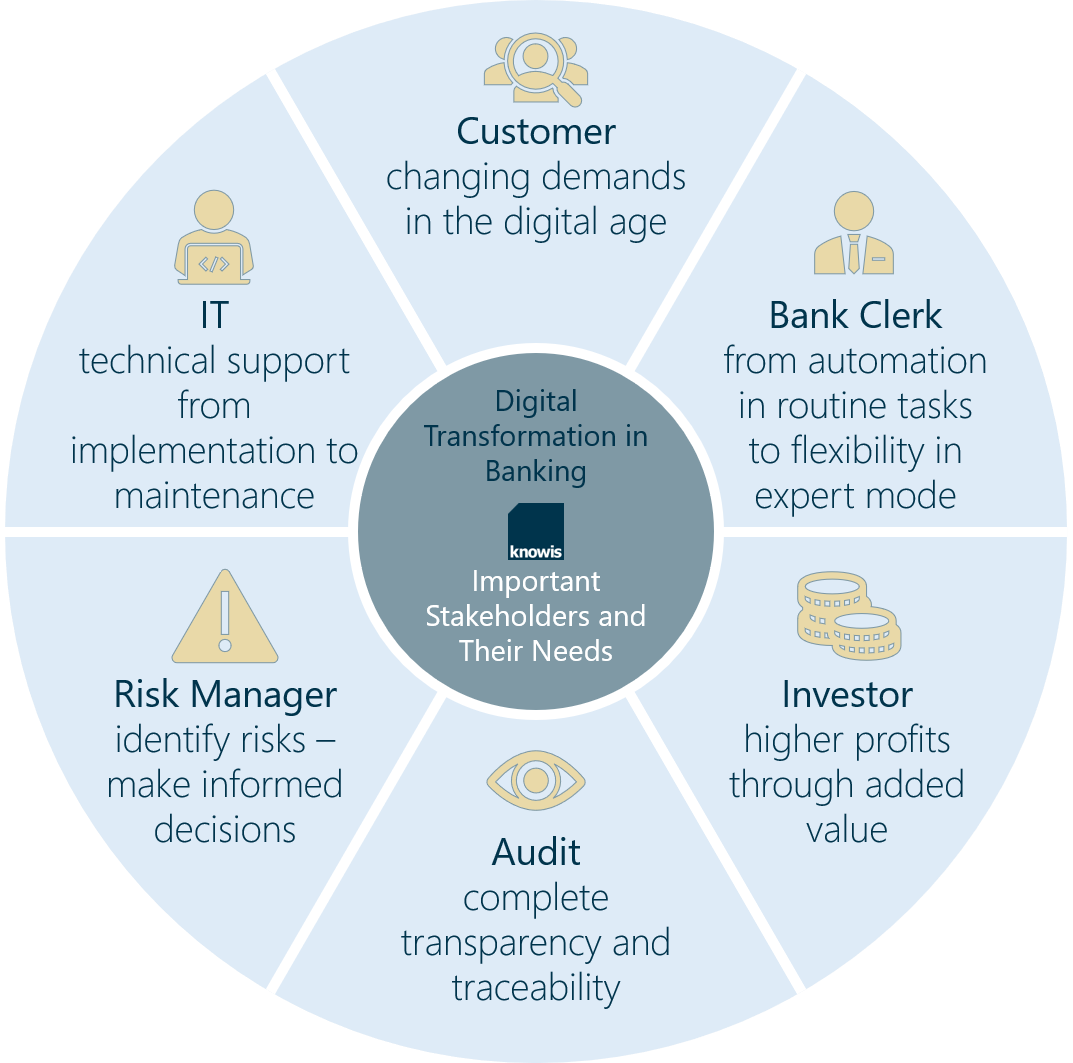

Key stakeholders in the Banking and credit environment and their needs

There are many people and groups of interest who are important for the success of a digitalization project in banking and credit. These vary depending on the size and orientation of the financial institution and the type and scope of the project. However, some fundamental stakeholders can be found in almost every project of digital transformation:

The bank customer - changed demands in the digital age

In recent years, customers have become familiar with digital processes in many areas of life and have become correspondingly expectant. Today, these expectations go beyond things that have become a matter of course, such as mobile user interfaces or 24/7 availability of information, even in the financial sector. Topics such as the transparency of processes, the comparability of offers, or a stronger integration into the process are becoming increasingly important.

The focus is on the positive user experience of individual customers, even outside the bank counter:

- Availability of the relevant data via all communication channels (online portals, mobile apps, at the agent on site), as well as the switching of channels without loss of information: Omnichannel-Banking

- Individual and innovative products that are precisely tailored to the respective customer needs

- Consistent digital customer experience, i.e. a seamless flow of information from initial contact to existing customer care

Bank Clerk - From routine tasks to expert mode

The interests of the clerk overlap in many ways with those of the customer. The fast and reliable availability of information and customer data is also important to him. By linking information across applications, he wants to save time and avoid errors.

The most important requirements can be summarized in this way:

- No time-consuming system changes within the machining process

- On the one hand automation/support for routine work, on the other hand individual freedom for processing if necessary

- Access to comprehensive structured information in context with the customer relationship

Investors - More value through added value

In the interests of the company, the investors carefully consider whether investments in a new technology are worthwhile. They do not have to be convinced by features, but by facts. They are particularly interested in how the digitalization project will affect the profitability of the company. The questions about the expected increase in efficiency, the planned project period, and the personnel required are obligatory.

In this context, it is also worth taking a closer look at medium to long-term prospects:

- How good is the system flexibility when adjustments are required, for example, due to regulatory changes or internal process optimizations?

- Is the used technology fit for future demands, does it offer the necessary interfaces and cloud functionalities?

- Will the company be enabled to strengthen sales, for example by connecting an online platform to the existing systems?

Regulator / Audit - Complete transparency and traceability

As a guardian of regularity, the audit has the function of examining facts independently and objectively. It must determine whether set standards and regulations are being observed in the prescribed manner. The requirements arising from this are reflected, among other things, in topics such as a non-manipulable database and reliable archiving.

To ensure a high level of stakeholder value in the audit area, particular attention should be paid to these areas:

- Management and assignment of roles and authorizations, support in compliance with the need-to-know principle

- Complete documentation and historicization of the underlying data and facts

- Features for fast and uncomplicated evaluations and analyses

Risk Manager: Identify risks at an early stage, decide in a differentiated manner

The identification and assessment of risks is a central task of the lending business. In times of growing regulation, this task is more important than ever and is also taking up more and more space within bank management. A reliable database as a basis for reliable results and an appropriate risk assessment is therefore also of great importance for this interest group.

The main focus of a risk-oriented audit and assessment:

- Instruments for early/automated identification of risks and risk tendencies

- Possibilities to create risk filters and carry out risk-adjusted evaluations

- Simplification of approval and decision-making processes in the sense of differentiated and risk-oriented decision making

IT management: Plannability from implementation to maintenance

The IT management of the financial institution of course views digitalization projects from a very technical perspective. In addition to planning and supporting the technical implementation, aspects such as IT security and maintainability after completion of implementation are also in the focus of this interest group.

Further important criteria from the IT point of view are:

- To keep the effort for the integration of existing systems as low as possible without having to make adjustments to the existing systems themselves

- Meet all security standards, both locally and in the cloud

- Easy extensibility for follow-up projects

Conclusion

There are many points of contact with different interest groups when implementing a digitalization project in the banking sector. All of them ultimately decide whether a project will be implemented at all, what scope it will have, and how successful it will be in the long term. Therefore, it must be the aim of those responsible for the project to know the stakeholders and their interests at an early stage and to consider them in the various phases of implementation.

Image Sources: Teaser: courtneyk - 1008090940 - iStock; Infographic: knowis AG