'If it ain’t broke, don’t fix it' – this wisdom is no longer good advice for banks when it comes to their IT systems. Many core banking systems no longer meet current technical and security standards and, through numerous extensions, have become so complex that they hamper digital transformation and growth. The IT structure, which has grown over decades, has developed into an expensive heritage.

Inefficient, sluggish and obsolete: this is what the core banking systems, and thus the technological hearts of many financial institutions, look like. At the same time, exactly the opposite is demanded of banks: buzzwords like PSD2 and Open Banking are now mentioned in the same breath as speed, flexibility and collaboration. Increased competition and strict regulations make it impossible for banks to continue relying on legacy systems from the past century.

What are Legacy Systems and What do They Have in Common With Spaghetti?

We usually mean older existing systems or historically grown system landscapes in companies when we use the term 'legacy systems'. That sounds a bit dated and often it is: the existing technology no longer meets the current standards. Nevertheless, these established systems create significant value through their wide range of functions and enormous amounts of inventory data. Their contribution to added value can only be transferred to modern operating environments with tremendous effort.

Modernization efforts become particularly problematic if the legacy is made up of proprietary monolithic systems with an outdated operating or development environment. Continuous extensions with new features and stand-alone solutions, as well as interfaces to other applications in legacy IT, have often created a jumble of dependencies over the years, with no transparent structure or logic. This increases the complexity and leads to an intricate system landscape that resembles a plate of spaghetti. An uncomplicated migration to new versions or other providers is hardly possible.

The Core Banking Systems – A Heavy Legacy for Many Banks

Financial institutions have to cope with the increased need for action too, triggered by the obligation to migrate because of the vendor's discontinuation of support, new regulations from the supervisory authority, or digitization projects that are not feasible with outdated systems. Their legacy is the core banking systems. Among other things, this technical infrastructure manages extensive customer data and maps and processes banking operations such as account management, loans and savings deposits.

Many of the core banking systems still in operation were created in the 1970s during the first wave of digitization in banking, so their ability to integrate new technologies is correspondingly limited or cumbersome. In order to still meet the changing requirements of the market, financial institutions have attempted in recent decades to provide process workarounds, software modifications, or additional isolated components that were not provided for in the originally specified functionality of their core banking systems. In most cases, these custom solutions were not interoperable, which made the IT systems more and more opaque and complex.

Although they used to be IT pioneers, financial institutions have thus been building technical debt for decades; today they have to bear the consequences of historically grown, not very stringent implementation.

Why Obsolete Technology Threatens the Future of Banks

Owing to the organic development of the legacy system, the initial software architecture is hardly recognizable. Instead of a modular structure, everything is mixed into a "big ball of mud" that halts innovation and makes the integration of modern technologies and solutions, such as cloud computing, almost impossible.

The customer today has service expectations that require consistently digital channels and data processing in real time. However, legacy core banking systems are not directly connected to the customer interfaces, making cross-channel data flow impossible. In addition, these legacy systems often work batch-based, meaning that they complete tasks in batches at specific intervals, which may take several hours. Thus, the banks often have no other solution than to manually control individual processes internally in order to simulate a rudimentary omni-channel journey to the outside world. Nevertheless, this does not resolve the actual problem and leaves employees and customers unsatisfied in many areas.

The aging technologies are now finally reaching their limits. On the one hand, this is reflected by performance problems and lack of flexibility in the development of new business models; on the other hand, the legacy systems often no longer meet current security standards. Last but not least, further development and maintenance is complicated and costly, because developers with programming skills for the old IT landscapes are becoming scarce.

What Does a Modern IT System for Banks Look Like?

PwC makes it clear in their study Financial Services Technology 2020 and Beyond: Embracing Disruption – three of the six priorities that financial institutions should adopt as quickly as possible are related to a well thought-out core banking modernization and the use of modern software architecture: Upgrading the IT operating model to fit new digital standards, the preparation of an IT architecture that can adapt to changing requirements and reducing costs by simplifying legacy systems.

PwC makes it clear in their study Financial Services Technology 2020 and Beyond: Embracing Disruption – three of the six priorities that financial institutions should adopt as quickly as possible are related to a well thought-out core banking modernization and the use of modern software architecture: Upgrading the IT operating model to fit new digital standards, the preparation of an IT architecture that can adapt to changing requirements and reducing costs by simplifying legacy systems.

The consulting firm advises banks to update their IT operating model. As the system structure has grown wild over the years, there is no uniform database for applications. The implementation of workarounds as a supposedly fast solution makes the system even more complex. In order to adapt to new digital standards and respond to constant technological change, banks need a viable IT.

In addition, the architecture should be prepared to connect with everything and everywhere. Open Banking is the motto. Using interfaces (APIs), the bank can become the center of an ecosystem. The seamless exchange of information via API within system landscape makes it easier to integrate new products and services.

Finally, the study underscores the simplification of legacy systems as an important to-do. Complexity and the costly maintenance of core systems prevent financial institutions from staying competitive in the long term. By taking measures themselves to modernize their infrastructure or by relying on viable third-party software solutions, banks can more flexibly respond to market demands and effectively reduce costs. At the same time they lay the foundation for cloud-based services and software models and the introduction of AI technologies.

From this, financial institutions can derive the following recommendations for action:

- Modularization of the software architecture: Modern banking IT systems consist of a small-scale business architecture that has a modular structure. It is implemented by container technologies, microservices and APIs. This allows banks to react more flexibly to market requirements.

- Standardization via APIs: Initiatives, such as the Banking Industry Architecture Network (BIAN), help define the standards for software architecture, encapsulate banking systems correctly and increase interoperability.

- Reduction of complexity: Extracting step-by-step business logic from the core banking systems prepares the ground for a smooth legacy replacement. Only through this simplification will it be possible for banks to embark on crucial digitization initiatives.

This is How Banks Overcome Their Legacy Issues

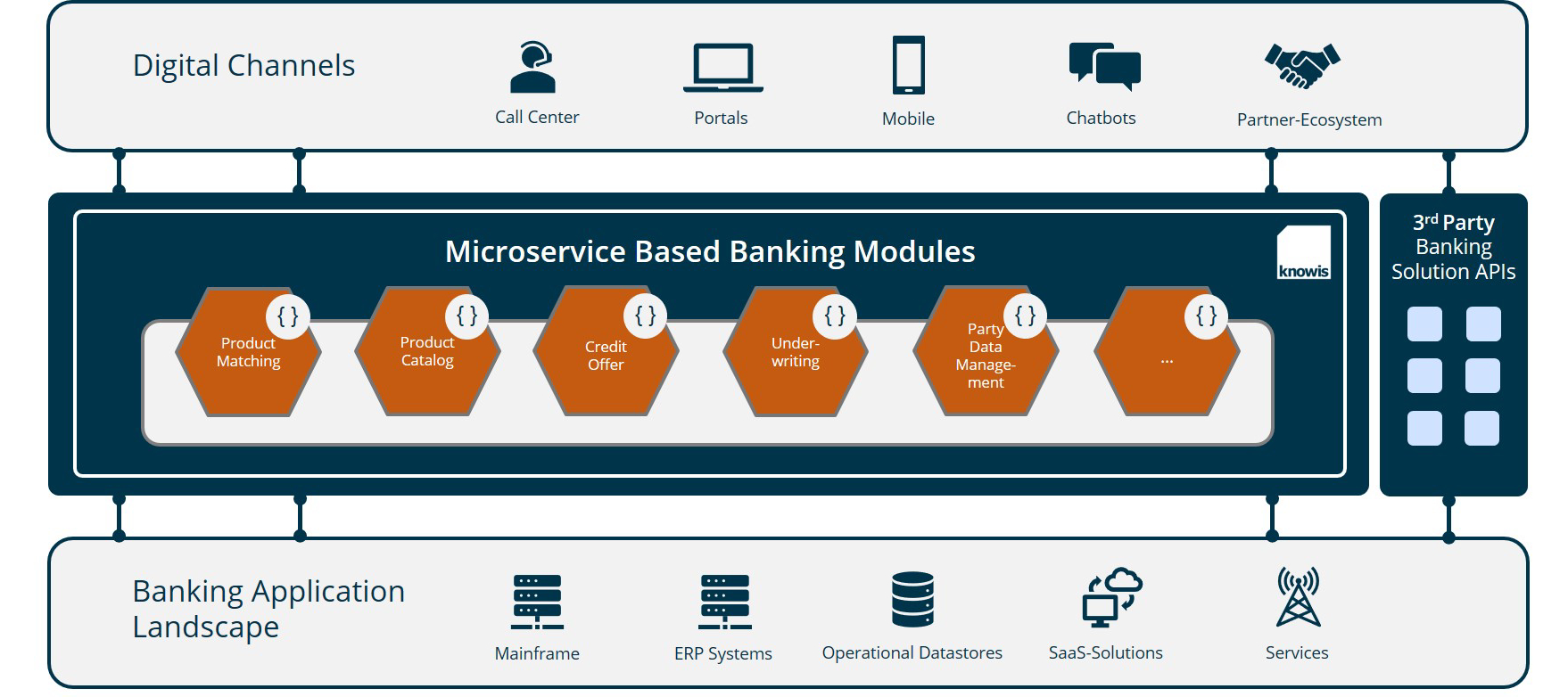

How do banks put the described recommendations for the transformation of their legacy into practice? By shifting the critical components of core banking systems, such as intelligence and business logic, to a higher-level platform, banks can decide for themselves how, and at what speed, they want to modernize. The core itself remains unchanged and is extended by the platform – with solution modules that gradually replace the functionalities of the obsolete core banking systems. At the same time, such a banking platform, which is positioned above the existing systems like a dynamic layer, is the starting point for integrating modern technologies.

By building a microservices architecture based on the principle of self-contained systems (SCS), a modularization of the software architecture can be achieved. According to the SCS principle, each module is implemented as a stand-alone system, which is loosely coupled to other modules. Thus, the development or modification of individual areas can take place without affecting other systems. Via APIs, the individual SCS not only communicate with each other, but also with external channels. Industry models such as BIAN or IBM Information FrameWork (IFW) serve as a guide to achieve a rapid implementation.

In this way, the business processes of the core banking systems can gradually be outsourced and the complexity in the legacy system can be reduced. There is a gradual transition of functionality into a new agile environment until the core system is free of logic and joins. The banking platform becomes the central interface, the core banking system interchangeable.

Conclusion

Banks face many challenges: changing competition, regulations and rising customer expectations are just some of them. At the same time, there are also new technologies that meet exactly these requirements.

A modernization of the core banking systems is the basis for integrating such forward-looking technologies into IT systems. Banks therefore need a strategy to replace obsolete systems over the long term. Platform banking based on modular software architecture is an efficient way to create a new solution and provide a dynamic foundation that makes financial institutions competitive and future-proof.

Image sources: Teaser: sjharmon - 540517348 - iStock; Infographic: knowis AG.