There is hardly a report on economic development without the catchphrase 'digital transformation'. The core message: Those who do not digitize are not fit for the future. However, to seize the real opportunity, it is not enough to replace paper-based forms with their digital counterparts. Rather, the goal should be to question and improve current conditions, taking into account state-of-the-art technology and industry standards.

A successful and sustainable digital transformation must therefore be geared primarily to the needs of the respective stakeholders and the long-term business objectives. The technological foundation should be highly flexible, as both markets and technologies will undergo increasingly rapid change in the future.

In the context of the lending business, this means more than just transferring paper-based documents or Word and Excel templates for a credit application into a digital format. Stakeholders have far greater demands; not least because there are far more technology choices today, which in many cases have already become an integral part of other areas of life. This includes, in particular, the design of appealing omni-channel customer journeys, the utilization of automation potential, and complete transparency of information.

Digital transformation holds enormous potential for banks, especially in the credit sector. Processes centered around credit are complex and intricate. There is often no precise knowledge of their profitability. Focusing on the interests of the stakeholders quickly reveals that, in the current situation, significant improvements can be achieved for all participants through continuous and flexible digitization of credit processes.

From a technological point of view, the subject matter should be embedded in the Digital Agility Layer when establishing platform banking so that existing solutions can be integrated seamlessly. It is also crucial for us in digitization projects to speak the customer’s professional language in order to clearly identify the problems, expectations and wishes of the stakeholders. After all, the solution is supposed to solve real and complex tasks in the lending business.

From a technological point of view, the subject matter should be embedded in the Digital Agility Layer when establishing platform banking so that existing solutions can be integrated seamlessly. It is also crucial for us in digitization projects to speak the customer’s professional language in order to clearly identify the problems, expectations and wishes of the stakeholders. After all, the solution is supposed to solve real and complex tasks in the lending business.

By using Domain-Driven Design (DDD), business expertise is becoming the focus of joint solution development. The business domains and their contexts are used as a common, interdisciplinary language to model functional solutions. Misunderstandings between developers and credit experts are thereby avoided.

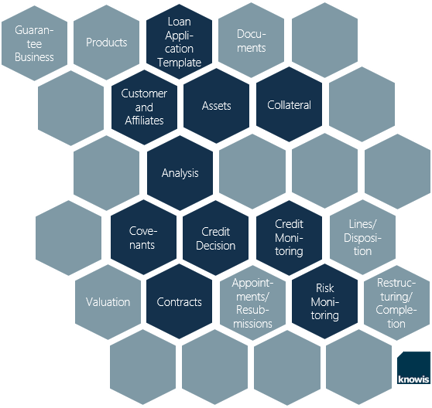

Within a banking platform, modular solution components whose boundaries are defined by business domains allow for a flexible response to shifts of the market and changing business needs; additionally, they facilitate fast release cycles. The individual components are developed, managed and controlled independently. Although being clearly distinct, they can exchange knowledge and data, providing the foundation for successful business automation and the future deployment of cognitive technologies.

Within a banking platform, modular solution components whose boundaries are defined by business domains allow for a flexible response to shifts of the market and changing business needs; additionally, they facilitate fast release cycles. The individual components are developed, managed and controlled independently. Although being clearly distinct, they can exchange knowledge and data, providing the foundation for successful business automation and the future deployment of cognitive technologies.

The solutions accumulate to a flexible and powerful credit architecture that can respond dynamically to changes resulting from altered internal or regulatory requirements. This modular approach also pays off in terms of the duration and expense of digitization projects.

In our experience, the solution components marked in the picture are sensible starting points for the structuring and development of a credit architecture – the individual design and the application spectrum of the individual modules remain unaffected. This type of solution configuration using existing solution modules, templates and patterns ensures the necessary flexibility and a short time-to-market.